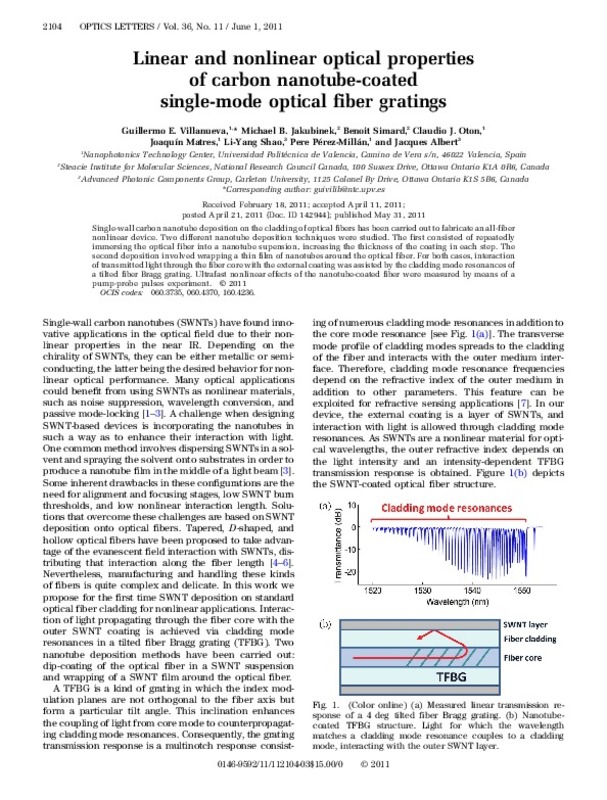

Numerical analysis and computing of a non-arbitrage liquidity model with observable parameters for derivatives

RiuNet: Repositorio Institucional de la Universidad Politécnica de Valencia

JavaScript is disabled for your browser. Some features of this site may not work without it.

Buscar en RiuNet

Listar

Mi cuenta

Estadísticas

Ayuda RiuNet

Admin. UPV

Numerical analysis and computing of a non-arbitrage liquidity model with observable parameters for derivatives

Mostrar el registro sencillo del ítem

Ficheros en el ítem

| dc.contributor.author | Casabán Bartual, Mª Consuelo

|

es_ES |

| dc.contributor.author | Company Rossi, Rafael

|

es_ES |

| dc.contributor.author | Jódar Sánchez, Lucas Antonio

|

es_ES |

| dc.contributor.author | Pintos Taronger, José Ramón

|

es_ES |

| dc.date.accessioned | 2017-03-13T08:29:57Z | |

| dc.date.available | 2017-03-13T08:29:57Z | |

| dc.date.issued | 2011 | |

| dc.identifier.issn | 0898-1221 | |

| dc.identifier.uri | http://hdl.handle.net/10251/78691 | |

| dc.description.abstract | [EN] This paper deals with the numerical analysis and computing of a nonlinear model of option pricing appearing in illiquid markets with observable parameters for derivatives. A consistent monotone finite difference scheme is proposed and a stability condition on the stepsize discretizations is given. © 2010 Elsevier Ltd. All rights reserved. | es_ES |

| dc.description.sponsorship | This paper has been supported by the Spanish Department of Science and Education grant DPI2010-C02-01. | |

| dc.language | Inglés | es_ES |

| dc.publisher | Elsevier | es_ES |

| dc.publisher | Pergamon | es_ES |

| dc.relation.ispartof | Computers and Mathematics with Applications | es_ES |

| dc.rights | Reconocimiento - No comercial - Sin obra derivada (by-nc-nd) | es_ES |

| dc.subject | Nonlinear partial differential equation | es_ES |

| dc.subject | Numerical analysis | es_ES |

| dc.subject | Option pricing | es_ES |

| dc.subject | A-stability | es_ES |

| dc.subject | Discretizations | es_ES |

| dc.subject | Finite difference scheme | es_ES |

| dc.subject | Non-linear model | es_ES |

| dc.subject | Nonlinear partial differential equations | es_ES |

| dc.subject | Stepsize | es_ES |

| dc.subject | Differentiation (calculus) | es_ES |

| dc.subject | Economics | es_ES |

| dc.subject | Nonlinear analysis | es_ES |

| dc.subject | Nonlinear equations | es_ES |

| dc.subject | Partial differential equations | es_ES |

| dc.subject.classification | MATEMATICA APLICADA | es_ES |

| dc.title | Numerical analysis and computing of a non-arbitrage liquidity model with observable parameters for derivatives | es_ES |

| dc.type | Artículo | es_ES |

| dc.type | Comunicación en congreso | |

| dc.identifier.doi | 10.1016/j.camwa.2010.08.009 | |

| dc.relation.projectID | info:eu-repo/grantAgreement/MICINN//DPI2010-20891-C02-01/ES/MODELIZACION Y METODOS NUMERICOS, ALEATORIOS Y DETERMINISTAS, PARA EL FILTRADO DE PARTICULAS DIESEL EN MOTORES DE COMBUSTION INTERNA SOBREALIMENTADOS/ | es_ES |

| dc.rights.accessRights | Abierto | es_ES |

| dc.contributor.affiliation | Universitat Politècnica de València. Instituto Universitario de Matemática Multidisciplinar - Institut Universitari de Matemàtica Multidisciplinària | es_ES |

| dc.contributor.affiliation | Universitat Politècnica de València. Escuela Técnica Superior de Ingenieros de Caminos, Canales y Puertos - Escola Tècnica Superior d'Enginyers de Camins, Canals i Ports | es_ES |

| dc.contributor.affiliation | Universitat Politècnica de València. Facultad de Administración y Dirección de Empresas - Facultat d'Administració i Direcció d'Empreses | es_ES |

| dc.contributor.affiliation | Universitat Politècnica de València. Escuela Técnica Superior de Ingeniería Agronómica y del Medio Natural - Escola Tècnica Superior d'Enginyeria Agronòmica i del Medi Natural | es_ES |

| dc.description.bibliographicCitation | Casabán Bartual, MC.; Company Rossi, R.; Jódar Sánchez, LA.; Pintos Taronger, JR. (2011). Numerical analysis and computing of a non-arbitrage liquidity model with observable parameters for derivatives. Computers and Mathematics with Applications. 61(8):1951-1956. doi:10.1016/j.camwa.2010.08.009 | es_ES |

| dc.description.accrualMethod | S | es_ES |

| dc.relation.conferencename | 3rd International Symposium on Nonlinear Dynamics | |

| dc.relation.conferencedate | September 25-28, 2010 | |

| dc.relation.conferenceplace | Shanghai, China | |

| dc.relation.publisherversion | http://dx.doi.org/10.1016/j.camwa.2010.08.009 | es_ES |

| dc.description.upvformatpinicio | 1951 | es_ES |

| dc.description.upvformatpfin | 1956 | es_ES |

| dc.type.version | info:eu-repo/semantics/publishedVersion | es_ES |

| dc.description.volume | 61 | es_ES |

| dc.description.issue | 8 | es_ES |

| dc.relation.senia | 206963 | es_ES |

| dc.contributor.funder | Ministerio de Ciencia e Innovación |

Este ítem aparece en la(s) siguiente(s) colección(ones)

Ítems relacionados

Mostrando ítems relacionados por Título, Autor, Creador y Palabras clave.

Universitat Politècnica de València. Unidad de Documentación Científica de la Biblioteca (+34) 96 387 70 85 · RiuNet@bib.upv.es

El contenido de este sitio está bajo una licencia Creative Commons Reconocimiento – No Comercial – Sin Obra Derivada (by-nc-nd), salvo que se indique lo contrario.

Los metadatos de este sitio están bajo una licencia Dominio Público.